Canara ai1 Pay Cashback Offer 2026: Get ₹10 Daily on Merchant Scans

✍️ Author: Asish Khamaru (✅ Finance Educator) | 🛡️ Focus: Reliable Digital Earnings

Let’s talk about the current reality of UPI payments in 2026. If you use the massive, private third-party apps for your daily transactions, you probably know the frustration of receiving a "Better Luck Next Time" message or an expiring coupon for an app you never use. If you are constantly tracking the latest UPI cashback offers, you are likely aware that the era of giant, unconditional cashbacks from private aggregators is largely over. They have captured the market, and their customer acquisition budgets have shifted.

However, the new players entering the aggressive cashback space are the traditional banks themselves. To encourage users to utilize their proprietary digital ecosystems instead of relying on third-party apps, government and private banks are directly subsidizing transactions. One of the most consistent campaigns running right now is the Canara ai1 Pay Cashback Offer.

This is not a scheme that promises you thousands of rupees overnight. Instead, it is a highly reliable micro-earning system. By simply routing your daily, unavoidable expenses (like buying milk, paying for a rickshaw, or grabbing tea) through the Canara ai1 application, you can secure a small but guaranteed daily fiat return. In this comprehensive guide, I will break down exactly how to qualify for this campaign, the specific rules regarding merchant scans, and how to maximize this offer over a 30-day cycle.

- 1. Why Are Banks Giving Cashbacks Now?

- 2. Understanding the Canara ai1 Super App

- 3. Decoding the ₹10 Daily Cashback Engine

- 4. Step-by-Step Execution Protocol

- 5. The "Merchant Only" Rule Explained

- 6. Settlement: Where Does the Money Go?

- 7. Troubleshooting: Why Did My Cashback Fail?

- 8. Pros and Cons of Bank-Backed Offers

- 9. Final Verdict: Is it Worth the Effort?

- 10. Strict Financial Disclaimer

- 11. Frequently Asked Questions (FAQs)

1. Why Are Banks Giving Cashbacks Now?

To understand why this offer exists, you need to look at the backend of the Indian banking system. When you use a third-party app to scan a QR code, your bank bears the server cost of processing that transaction, but the third-party app gets the data and the user engagement. This infrastructure cost without any upside is hurting traditional banks.

To counter this, banks like Canara are heavily promoting their own "Super Apps." By paying you a small reward of ₹5 or ₹10 to use their app instead, they save on third-party server load and keep you actively engaged within their own banking ecosystem. This is a strategic operational budget, not a random giveaway.

2. Understanding the Canara ai1 Super App

Canara ai1 is not just a basic UPI scanner. It is an integrated banking application designed to handle over 250 features, from managing your savings account and booking fixed deposits to paying taxes and handling mutual funds.

💡 Do I Need a Canara Bank Account?

This is the most common misconception. No, you do not need a Canara Bank savings account to use the Canara ai1 UPI feature. Just like BHIM or other payment apps, the Canara ai1 app allows you to link any Indian bank account (SBI, HDFC, ICICI, etc.) that is registered with your mobile number to process UPI transactions.

3. Decoding the ₹10 Daily Cashback Engine

The mechanics of this promotional campaign are straightforward, focusing on building daily habits rather than offering a one-time jackpot.

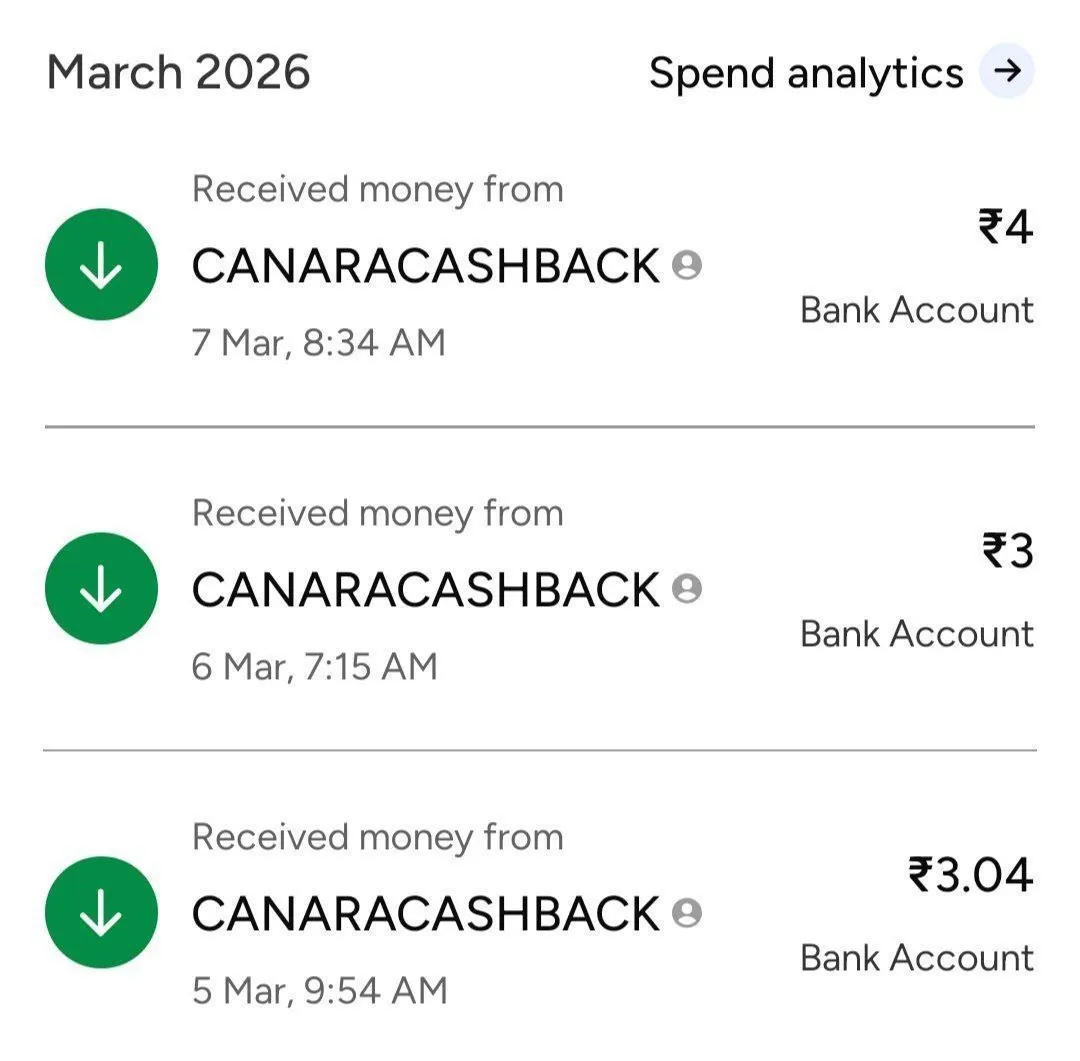

When an eligible user opens the Canara ai1 application and executes a payment of ₹30 or more by scanning a verified merchant QR code, the backend algorithm processes a cashback reward. Based on current campaign data, this reward fluctuates between ₹3 and ₹10. While this sounds small, doing this consistently for 30 days may help reduce small daily payment costs over time just for paying for things you were going to buy anyway.

4. Step-by-Step Execution Protocol

To ensure your transaction is registered correctly by the promotional algorithm, follow this daily routine:

- Installation: Download the official "Canara ai1 - Mobile Banking App" from the Play Store or App Store.

- Registration: Open the app and complete the SMS verification process using the mobile number linked to your primary bank account.

- UPI Setup: Navigate to the UPI section and link your preferred bank account. Set up or verify your standard 4 or 6-digit UPI PIN.

- The Transaction: Tap the "Scan & Pay" button. Point your camera at a physical merchant QR code at a local store.

- Amount Entry: Enter an amount of ₹30 or higher. Do not split payments artificially, as algorithms often flag rapid, repeated small transactions.

- Execution: Enter your PIN and complete the payment. If eligible for that day, the cashback will process immediately.

5. The "Merchant Only" Rule Explained

This is the critical failure point for most users attempting to claim this offer. The Canara ai1 system strictly monitors the type of QR code you are scanning.

If you scan your friend’s personal QR code or send money directly to a phone number (Peer-to-Peer or P2P), the transaction will process normally, but you will not receive any cashback. The reward is exclusively allocated for Peer-to-Merchant (P2M) transactions. This means you must scan the official business QR codes (usually the printed standees) found at grocery stores, pharmacies, petrol pumps, or online payment gateways.

6. Settlement: Where Does the Money Go?

Unlike third-party applications that force you to claim scratch cards that often result in useless discount coupons, the Canara ai1 application provides highly liquid fiat returns.

When the transaction is successful and the algorithm allocates your ₹3 to ₹10 reward, the fiat amount is routed directly via NPCI channels into the primary bank account you linked to the application. There are no closed-loop wallets, no minimum withdrawal limits, and no points to convert. It is direct cash deposited to your ledger.

7. Troubleshooting: Why Did My Cashback Fail?

If you scanned a code, paid ₹30, and received nothing, it is likely due to one of these parameters:

- Personal QR Scan: As detailed above, you scanned a friend's personal receiving code instead of a registered business/merchant QR.

- Daily Cap Reached: The campaign generally rewards only the first qualifying transaction of the day. Subsequent transactions on the same day will not yield additional cashback.

- Minimum Threshold Missed: You paid ₹25 instead of the mandated minimum of ₹30.

- Campaign Pause: Bank budgets fluctuate. If the monthly marketing budget is exhausted, the algorithm pauses the cashback dispensation until the next cycle.

8. Pros and Cons of Bank-Backed Offers

✅ Practical Advantages

- Rewards are highly liquid; direct fiat deposit into your primary bank account.

- Operated by a highly secure, RBI-regulated banking institution, ensuring maximum data privacy.

- Builds a consistent, daily micro-earning habit without requiring extra spending.

❌ Realistic Limitations

- The absolute monetary value is small (₹3 to ₹10 per day).

- Strictly limited to Merchant QR codes (P2M), reducing utility for peer-to-peer transfers.

- The app interface can occasionally be slower than dedicated third-party payment processors.

If you are looking for larger payouts, you might want to combine this daily habit with some of the best refer and earn apps available in the market.

9. Final Verdict: Is it Worth the Effort?

If you are expecting to make thousands of rupees overnight, this campaign is not for you. However, if you are a disciplined digital consumer who regularly purchases daily essentials via UPI, not utilizing this app means missing a potential promotional benefit. For more verified opportunities like this, always keep an eye on our latest active campaigns.

By simply replacing your current payment app with Canara ai1 for your first transaction of the day at the local dairy or grocery store, you may provide a small promotional cashback depending on campaign eligibility. It requires zero extra investment, zero complicated referral networking, and deposits pure fiat cash into your account.

⚠️ Financial & Campaign Disclaimer

This comprehensive review is provided strictly for educational and informational purposes based on current application testing. Bank-backed promotional campaigns are highly dynamic and are subject to immediate modification, suspension, or termination based on internal marketing budgets and user eligibility algorithms. The exact cashback values may fluctuate. Always refer to the "Offers" section within the official Canara ai1 application for the most up-to-date terms and conditions.

11. Frequently Asked Questions (FAQs)

1. Do I need a Canara Bank account to claim this offer?

No. The Canara ai1 app functions as a universal UPI interface. You can link any active Indian bank account (like SBI, Axis, or HDFC) that is registered to your mobile number and still qualify for the merchant payment cashbacks.

2. Why didn't I get cashback when I sent money to my friend?

The promotional algorithm specifically filters out Peer-to-Peer (P2P) transfers to prevent system abuse. To trigger the cashback, you must scan a registered Merchant QR code (P2M), such as those found at physical retail shops or online business checkouts.

3. Is there a daily limit on how many times I can earn the cashback?

Yes. Bank promotional campaigns generally restrict rewards to the first qualifying transaction of the day per user account. Executing ten consecutive ₹30 transactions to the same merchant will not yield ten separate cashbacks.

💸 Payment Proofs

100% VERIFIED

Swipe to see more

Official Telegram

Short-time loot aur 100% verified earning tricks sabse pehle paane ke liye join karein Like Offer Official! 💎

Join Community Now